The first quarter of 2026 was marked by significant volatility that continues to reverberate across global markets. The backdrop has been characterized by pronounced dispersion across equity sectors and individual stocks. The global economy entered 2026 following a 2025 "soft landing" supported by AI spending and fiscal stimulus, but Q1 brought heightened geopolitical risks alongside growing fears that AI spending plans may be unsustainable.

Markets continued to navigate the fallout from a series of geopolitical events, from the United States' interventions in Venezuela and Greenland in January, to the conflict in Iran and broader Middle East tensions. The impact on energy markets has been severe: Brent crude has nearly doubled and WTI is up approximately 80%. Natural gas has been similarly affected. The conflict in Iran has done more than disrupt oil flows; it has fractured critical nodes of the regional liquefied natural gas (LNG) supply chain in ways that may outlast the conflict itself. European gas prices have nearly doubled, and global interest rates are now pointing upward rather than down. That combination has likely left technology giants in a difficult position as they grapple with surging energy costs, adding further strain to an already pressured sector.

Portfolio weights remained approximately 51.8% Canadian equities and 43.7% US equities.

Oil was not the only commodity to make headlines. January saw the largest monthly rise in gold prices since the tail end of the global financial crisis. Yet gold has since fallen ~15% in March, putting it on track for its worst month since October 2008. In a quarter that has seen intensifying conflict in the Middle East as well as the most significant global energy shock in decades, this degree of volatility in a traditional safe-haven asset is noteworthy.

The AI boom continued to drive strategic investment in Q1, but the narrative may have shifted from exclusively optimistic to increased scrutiny over profitability as well as capex sustainability. Investors have become far more focused on distinguishing between potential winners and losers, and the possible threat of "disintermediation" as AI systems become more capable of handling repetitive and routine tasks has weighed on a range of industries in 2026, from legal services and insurance to freight logistics, property management, and most notably software stocks.

Private credit remained a key focus during Q1. The industry has grown rapidly over the past decade but has recently faced questions over valuation, transparency, and the broader health of the asset class amid rising defaults; this despite private credit executives continuing to maintain that loan portfolios remain sound. The sharp sell-off in software stocks has also drawn attention to the sector's exposure among less liquid and less transparent credit investors. While major firms reported record fundraising and deployment throughout 2025, Q1 2026 has seen a surge in redemption requests, mounting fears of AI-led disruption in software lending and increased regulatory scrutiny from global authorities adding to the overall volatile market environment.

Against this backdrop, equity markets have retreated from the highs reached in February but have not yet entered a full correction. The S&P 500 is down approximately 5% and the small-cap Russell 2000 is down around 0.5%. Elsewhere, the Nikkei 225 has declined 1.5%, the FTSE 100 is up 2.3% and the TSX60 is up 1.9%.

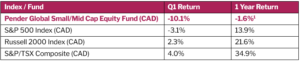

Fund specific updates (Q1 2026)

Kraken Robotics was the top performer in the quarter. Q1 was marked by a major strategic acquisition of Covelya Group Limited for $615 million. Covelya is an international provider of underwater technology solutions, and the acquisition enables Kraken to better bridge the gap between its core defense focus and the commercial subsea market. Overall, Kraken’s performance in the quarter was boosted by increased defense spending, as geopolitical tensions remain elevated and global interest in subsea drone technology and the protection of underwater infrastructure continues to grow.

Telesat was another top performer this quarter and remains one of our key Canadian defense holdings. In March, the company announced an important step in the commercialization of its Lightspeed LEO constellation. In response to growing demand from the Canadian Armed Forces and allied militaries, Telesat indicated it will allocate nearly a quarter of Lightspeed’s capacity to military Ka-band to support defence and sovereignty applications. Management also highlighted strong customer interest across its target markets, and we continue to see scope for additional commercial and strategic announcements this year. With several potential catalysts ahead, we believe Telesat remains an attractive holding with asymmetric upside.

Burford Capital saw its share price fall sharply after suffering a major legal reversal. On March 27, 2026, the 2nd US Circuit Court of Appeals overturned a $16.1 billion judgment against Argentina in a 2-1 decision, dealing a substantial blow to Burford's litigation portfolio. The case stemmed from Argentina's 2012 nationalization of YPF, at the time a privately held oil and gas company, which left minority shareholders without the buyout they were contractually owed, a claim Burford financed in exchange for a share of any eventual award The panel struck down the award granted in September 2023 by a lower court to former YPF shareholders, ruling that the plaintiffs' breach of contract claims failed under Argentine law. Burford which stood to collect a substantial portion of the award, suffered a major financial setback, with its shares dropping ~47% on the day. This was a low probability binary event and unfortunately it did not go the way we had anticipated. We remain confident in our overall process and have subsequently decided to exit the position in the Fund.

Coveo and Par both had challenging quarters as their stocks sold off alongside the broader software sector. We do not believe anything fundamental has changed in these businesses, and our investment theses remain unchanged.

David Barr, CFA

April 14, 2026

1 All Pender performance data points are for Class F of the Fund. Other classes are available. Fees and performance may differ in those other classes. Standard Performance Information for the Fund may be found here: https://penderfund.com/fund/pender-global-small-mid-cap-equity-fund/