Dear Unitholders,

The Pender Alternative Absolute Return Fund returned -2.0%1 in April, bringing year to date return to 1.1%.

The exceptionally strong bid for risk despite the ongoing and worsening disruption to global energy markets was a difficult set up for the Fund. Credit markets tapped out early in April even as equities continued to move higher. The typical high yield bond saw its price decline slightly from April 9 through the end of the month, while the S&P 500 Index added almost 400 points over the same period. The ICE/BofA US High Yield index returned 1.7% in the month, bringing year to date returns to 1.1% in USD.2

The HFRI Credit Index hedged to CAD, the Fund’s benchmark returned 1.8% in April, bringing year to date returns to 2.3%.

Portfolio & Market Update

The S&P 500 put up its best monthly return since November 2020 in April. Back then, markets celebrated the advance of an effective COVID-19 vaccine. While last month the catalyst seemed to be a technical bounce that was supercharged by trend-following strategies like Commodity Trading Advisors (CTAs), whose buying activity triggered technical signals to buy even more. The strength of the initial recovery was more consistent with a bounce of a 30% drawdown in equities rather than the 9% realized drawdown in the S&P.

Starting valuations are usually cheaper during sharp equity rallies. In previous instances where the S&P 500 rallied more than 10% in month, starting spreads for high yield were above the long run average (443bp over past 15 years), not close to cyclical lows like they were at the end of March. Momentum can only go so far in credit, while there are limited valuation guard rails for equities, with Intel hitting a P/E multiple of 84x their expected 2027 earnings in May.

Source: Bloomberg

We used strength in risk sentiment to sell most of our positions in Open Text Holdings Inc. (TSX: OTEX) bonds as well as several smaller positions in the Fund.

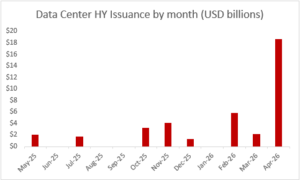

Very heavy AI data center issuance in April presented opportunities to deploy capital at significantly better rates than was available earlier in the year. An issuer backed by Tract Capital Management LP issued bonds in April which was nearly identical to a related structure that tapped the market in February, both helping fund the buildout of an “AI factory” in Nevada for NVIDIA Corp. (Nasdaq: NVDA) which has a long-term contract for the facilities. Once the facilities are constructed and stabilized we expect both issues will be rated investment grade.

Source: Bloomberg

At the close of business on the first day of trading, April’s issue had a yield more than 100bp higher than February’s. In February we quickly sold our allocation in the secondary market while we added to our position in April. We now have about 15% of the Fund invested in AI data center bonds, the vast majority of which are backed by long term leases from either NVDIA or Alphabet Inc (Nasdaq: GOOG).

The current wave of high yield data center issuance started in May of last year, when Coreweave Inc. (Nasdaq: CRWV) came to market with a senior unsecured issuance. Coming into April there was a total of just over $20 billion in data center bonds outstanding. This total almost doubled in a month, which was a lot for the market to digest and unlike any other capital investment wave we’ve seen in the past twenty years.

Source: PenderFund

We were able to recycle capital from selling bonds that had rallied in April into shorter duration energy holdings that we believe are likely to be called in the near term or have limited downside. One example is Saturn Oil and Gas Inc. (TSX: SOIL) 9.625% bond due in 2029 which will become callable at a price of $104.81 in June. We were able to grow our position from 1% to 3% of the Fund in April, all at a slight discount to the call price, generating an attractive short-term yield of over 9% to call.

While the strong price momentum in early April sent a signal to some investors that it was time to chase risk higher, our valuation driven approach argues the opposite. With high yield spreads in the vicinity of 280bp which is both historically expensive and a significant resistance level of the past couple of years, we believe that maintaining a defensive posture and waiting for trading opportunities is prudent.

Despite the frothy macro environment, there is plenty of bifurcation in markets today which we believe will present more individual trading opportunities than one would typically expect at these absolute valuation levels.

Market Outlook

Credit significantly underperforming equities in recent weeks should be seen as a warning sign for risk assets broadly. This is particularly relevant when considering how narrow breadth has been in equity markets, and that current equity market leadership is dependent on a credit funded capital expenditure cycle. Demand for high yield data center bonds was pushed to its limit in April, which has caused banks to pause bringing additional deals for now, but we expect that supply will ramp up again shortly.

While the market has been focused on semiconductors and the AI trade, the energy disruption at the heart of March’s market weakness has increased by some measures. JP Morgan estimates that the disruption to global oil supply widened from 9.1 million barrels per day in March to 13.7 million barrels per day in April. While inventories have provided a significant shock absorber so far, they are not a sustainable solution for this magnitude of disruption. If nothing changes, significantly higher energy prices will be required to incentivize demand destruction in the coming months. Current prices are already contributing to worsening inflation data in the United States. Data for April showed spikes in both consumer and producer prices that were above analysts' expectations. The PPI data was particularly hot and could be a forward indicator of consumer prices.

Equities and to a lesser extent credit markets have shrugged off rising yields in recent weeks, but we suspect that further increases in government bond yields will impact risk appetite and risk premiums. Despite the uniquely strong equity rally, we believe that risk assets are in a vulnerable position today, we remain well hedged for macro weakness as valuations leave little room for error.

Portfolio Metrics

The Fund finished April with long positions of 137.5% (excluding cash and T-bills). 37.0% of these positions are in our Current Income strategy, 97.8% in Relative Value and 2.7% in Event Driven positions. The Fund had a -69.1% short exposure that included -3.6% in government bonds, -42.8% in credit and -22.7% in equities. The Option Adjusted Duration was 1.67 years.

Excluding positions that trade at spreads of more than 500bp and positions that trade to call or maturity dates that are 2028 and earlier, Option Adjusted Duration declined to 1.28 years.

The Fund’s current yield was 6.43% while yield to maturity was 6.89%.

Justin Jacobsen, CFA

May 21, 2026

1 All Pender performance data points are for Class F of the Fund unless otherwise stated. Other classes are available. Fees and performance may differ in those other classes. Standard performance information for the funds can be found here: https://penderfund.com/fund/pender-alternative-absolute-return-fund/

2 Bloomberg