February was an interesting month for investors, marked by elevated volatility and significant return dispersion beneath relatively modest headline index moves. Market leadership continued to shift, and with geopolitical tensions rising into early March, volatility may remain a key dynamic as geopolitical tensions contribute to elevated global uncertainty.

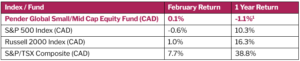

Portfolio weights remained approximately 56.7% Canadian equities and 42.2% US equities.

In US equities, elevated valuations in mega-cap technology names triggered bouts of selling pressure. The NASDAQ 100 declined -2.3% month-over-month while the S&P 500 fell -0.9%. At the same time, there were early signs of a broadening in market participation as investors began looking beyond the “Magnificent 7” toward smaller companies that appeared attractive with stronger earnings growth potential. Reflecting this shift, the Russell 2000 gained 1.0% during the month.

Artificial intelligence remains the dominant force shaping investor sentiment. Despite solid earnings results from large technology companies, investors are increasingly questioning the return on the enormous capital expenditures being announced by hyperscalers. More broadly, the perceived disruptive impact of AI has triggered sharp selloffs across a wide range of industries including software, logistics, financial data providers, commercial real estate services, and parts of the wealth management industry. In several cases, share prices have fallen 25%, 40%, or even 60% from recent highs.

The central question is whether these moves reflect lasting impairment to business models or whether markets are reacting more aggressively than fundamentals justify. At present, markets appear to be selling first and asking questions later. While disruption is real, history shows that industries often adapt and evolve as new technologies emerge. Our focus is not on reacting to headlines, but on identifying where markets may be confusing disruption risk with durable long-term opportunity.

The rotation in equity markets has also benefited more asset-heavy sectors tied to the buildout of AI infrastructure. Manufacturers, raw material producers, and other value-oriented industries have begun to outperform as investors position for the next phase of the AI investment cycle.

Commodity markets reflected similar dynamics. After correcting sharply at the end of January, precious metals rebounded strongly, returning 12.4% in February. In energy markets, rising US inventory levels weighed on prices through most of the month before escalating tensions in the Middle East caused oil prices to spike toward month-end.

We believe periods of volatility and rapid narrative shifts often create the most compelling investment opportunities. In an environment where markets are increasingly reacting to headlines and uncertainty, disciplined fundamental analysis becomes even more important. Our focus remains on identifying businesses with durable economics and long-term growth potential, particularly where short-term market reactions may be creating attractive entry points.

Fund specific updates (February)

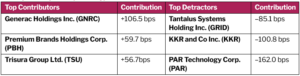

Generac was the top performing holding during the month. The company designs and manufactures energy technology solutions and backup power systems. While the residential generator business has historically driven growth, benefiting from increasing grid instability, the data center market is emerging as a major opportunity. As hyperscalers build AI infrastructure, demand for reliable backup power is rising. CEO Aaron Jagdfeld described the opportunity as “one of the biggest needle-moving opportunities” in his three decades with the company.

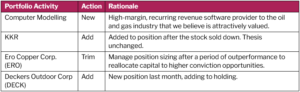

KKR and Co had a weak month as concerns around risks in the private credit market led to a broader sell-off, with KKR declining alongside peers such as Blackstone and Apollo amid a negative shift in sentiment. KKR has built one of the largest private credit platforms in the alternative asset management industry, with ~ $130 billion in private credit AUM as of late 2025. The sector has been under pressure following developments at Blue Owl Capital, and the overall health of the asset class has also been questioned amid rising defaults, although private credit executives continue to maintain that loan portfolios remain healthy. Our thesis remains unchanged. During the month, KKR reported full-year 2025 results and announced a $1.4 billion acquisition of Arctos Partners. As shown below, we added to our position, and KKR is now a top-10 holding.

Computer Modelling Group (CMG) was a new position initiated during the month. CMG is a specialized software company providing reservoir and seismic solutions to the global oil and gas industry. The company has historically generated attractive economics, supported by high margins, strong free cash flow, and a largely recurring revenue model. Based on our intrinsic valuation analysis, we believe CMG is trading below its fair value range, providing an attractive entry point as the company executes on its strategy to expand into a broader subsurface software platform.

David Barr, CFA

March 16, 2026

1 All Pender performance data points are for Class F of the Fund. Other classes are available. Fees and performance may differ in those other classes. Standard Performance Information for the Fund may be found here: https://penderfund.com/fund/pender-global-small-mid-cap-equity-fund/