Dear Unitholders,

The Pender Alternative Absolute Return Fund returned -0.4%1 in May, bringing year to date return to 0.7%.

Euphoric market conditions continued in May, as ever-increasing AI spending was celebrated by investors. Fixed income continued to lag as an uptick in US inflation and the ongoing disruption to energy markets proved to be a headwind for government bonds globally. High yield benefitted from a reprieve of data center issuance which had weighed on the market in late April.

The HFRI Credit Index hedged to CAD, the Fund’s benchmark returned 0.9% in May, bringing year to date returns to 3.0%.

Portfolio & Market Update

The pause in AI data center issuance resulted in a rally in our positions in the second half of May, allowing us to substantially reduce our exposure to the sector. We expect that there will be additional waves of issuance and opportunities for better entry points as the year progresses. Software also bounced in May as earnings from some issuers were more resilient than expected. We continued to trim our software exposure on strength as we expect the balance of the year to see sentiment and valuation swings and, in our view, we expect that the late May/early June spread levels will be near the tight end of trading ranges going forward.

Markets appear to have remained optimistic about a quick resumption of energy flows from the Middle East, where we have seen opportunities to deploy capital into high yield energy issuers in both our current income and relative value strategies. The Fund bought a new issue from Kraken Oil and Gas Partners LLC (private), which priced a 5-year USD bond at a yield of 7.125%, we added to the position below par. With low leverage of 1.2x EBITDA and a favorable commodity exposure we believe the bond represents good value relative to the broad market, regardless of what happens in the Middle East.

Hyperscalers continued to raise capital in credit markets in May, with Alphabet Inc. (GOOG) issuing the largest ever Canadian dollar corporate bond transaction at C$8.5 billion early in the month, only to be surpassed in June as Amazon.com Inc raised C$14 billion. We viewed Alphabet’s issue as attractive and participated in the 30-year bond on a duration hedged basis, before selling out of our position once the spread rallied. We did not participate in the Amazon issue due to a lack of new issue pricing concession. With global fixed income markets saturated with AI related issuance, it appears to be equity markets turn in June, which is a very significant regime shift from years of the market being supported by large share buyback programs, and could ultimately prove to be a catalyst for the recent divergence between credit and equity markets converging.

With high yield and equity markets diverging for close to two months, history has shown that credit is the leading indicator more often than not. With that in mind, and with spreads near historic tights we continue to be defensively positioned. Early in June there are indications that, in our view, the euphoric rise in asset prices over the past couple of months may have run out of momentum.

Market Outlook – It’s equities’ turn

The initial wave of AI capital spending by hyperscalers was funded from cash on hand and their prodigious cash flow streams. Once those sources were exhausted, they turned to credit markets which saw issuance pick up in a significant way last fall. AI and data center related issuance has surged in credit markets this year, but the need to fund spending has grown even further. This need for capital caused Alphabet Inc. to act early in June by announcing an $86 billion equity capital raise, $40 billion of it using an At The Money (ATM) equity program that isn’t expected to start until Q3. Alphabet front running SpaceX’s IPO as well as AI competitors Anthropic and OpenAI demonstrated that equity is now a critical component in the AI arms race for capital.

2026 could be the first year of positive net US equity supply (issuance less buybacks) in 23 years2, which is a major regime change. This does not include the removal of lock ups that typically happens six months after an IPO. If Coreweave is any guide, the coming wave of IPOs are likely to see significant insider sales once lock ups expire, which was also the case in the internet mania of the late 1990s.

Mark Twain once said that history doesn’t repeat itself, but it rhymes. In late 2024, we listened to an outstanding podcast In Good Company featuring Stan Druckenmiller speaking with Nicolai Tangen the CEO of Norges Bank Investment Management, the Norwegian sovereign wealth fund. In their conversation, Stan recalls how he traded the end of the internet bubble; he spoke about his junior traders making 4-5% in a day in internet stocks. This kind of price action seemed crazy to me when I first heard it in 2024, but seems somewhat pedestrian in the spring of 2026 when the US semiconductor index is frequently up 5% in a day. It bears remembering that those are not normal price moves for a market that should be rationally discounting a company’s long term cash flows.

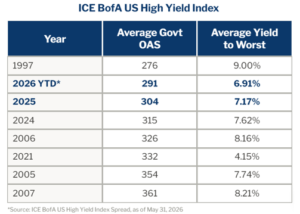

Credit markets today echo the extended periods of calm before market peaks from past cycles. At the current rate, 2026 will see the lowest average spread in the high yield market since 1997. The longer these periods go on, the larger the adjustment that is typically required when risk appetite shifts, often resulting in significant overshoots and compelling market opportunities. While timing this market exactly is impossible, it seems clear to us that we are seeing near peak investor behavior.

Portfolio Metrics

The Fund finished May with long positions of 135.6% (excluding cash and T-bills). 36.9% of these positions are in our Current Income strategy, 97.5% in Relative Value and 1.2% in Event Driven positions. The Fund had a -70.3% short exposure that included -3.7% in government bonds, -43.8% in credit and -22.8% in equities. The Option Adjusted Duration was 1.29 years.

Excluding positions that trade at spreads of more than 500bp and positions that trade to call or maturity dates that are 2028 and earlier, Option Adjusted Duration declined to 0.92 years.

The Fund’s current yield was 6.36% while yield to maturity was 6.57%.

Justin Jacobsen, CFA

June 17, 2026

1 All Pender performance data points are for Class F of the Fund unless otherwise stated. Other classes are available. Fees and performance may differ in those other classes. Standard performance information for the funds can be found here: https://penderfund.com/fund/pender-alternative-absolute-return-fund/