In February, the Fund delivered a return of 1.2%. The portfolio once again benefited from its resource holdings, which helped offset a challenging month for technology companies.

February was an eventful month, with AI disruption narratives continuing to drive significant drawdowns across software and IT services companies. The S&P 1500 Software and Services Index finished the month down 10% and is now down 22% year-to-date, marking its worst start to a year on record. Valuations for Canadian software consolidators also declined during the month, with EV/EBITDA multiples compressing meaningfully.

The AI theme evolved in February from broad enthusiasm to a more nuanced assessment of potential winners and losers, particularly within the small-cap universe. AI-related concerns impacted nearly all service-based sectors, with sentiment reaching peak pessimism amid narratives calling for the widespread displacement of knowledge workers. While the near-term environment remains volatile, we are increasingly excited about the opportunity set within the software sector, where the combination of improving businesses and compressed valuations is creating attractive opportunities for the Fund.

While the broader market faced headwinds from “sticky” inflation and concerns about AI disruption, the Russell 2000 gained 0.70% in a month when the Nasdaq 100 fell 2.30%, marking its worst monthly decline since March 2025. Meanwhile, with geopolitical tensions top of mind, the S&P/TSX Composite Index returned 7.7% in February. Within the index, Energy was the standout contributor, and small-cap performance during the month was largely underpinned by the strength of the resource complex.

Portfolio weights remain predominantly Canadian, with approximately 81.2% in Canadian equities and 13.8% in US equities.

Portfolio Holdings – Updates

Highlander Silver was a top performer and had a transformative February, highlighted by the successful closing of its acquisition of Bear Creek Mining. The transaction effectively positions the company as a multi-asset precious metals developer with a significantly expanded resource base. In addition to this major corporate milestone, the company secured strategic financing and received approval to list its common shares on the NYSE American LLC, with trading expected to commence on March 11. The company’s expansion comes amid a period of strong silver demand and price appreciation.

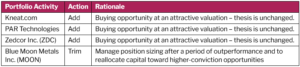

Kneat.com was a detractor this month, as it was caught up in the broader pessimism surrounding the software sector. That said, we remain confident in our thesis and view Kneat as a beneficiary of AI rather than facing existential risk from it. In the company’s full-year 2025 results, management highlighted meaningful progress in product innovation during February, particularly with the rollout of new AI features designed for highly regulated life sciences environments. Kneat continues to actively integrate AI capabilities both within its platform and across its internal operations, a strategy the company highlighted in its shareholder letter2. As shown below, we added to our position during the month based on this conviction, and the company remains a Top 10 holding in the portfolio.

Perspectives

As we look ahead, we continue to monitor opportunities where undervalued small-cap businesses with strong economic characteristics are trading at attractive valuations. In February, we continued leaning further into technology exposure, reflecting where we believe there are compelling long-term opportunities. The combination of improving business fundamentals and compressed valuations is the type of environment where long-term investment opportunities often emerge.

As a result, we have been selectively increasing exposure to technology businesses with recurring revenue models, strong margins, and long-term compounding potential. In our view, short-term price dislocations are not a flaw in the investment process, they are often the source of long-term opportunity.

The continued performance from our resource holdings has also provided a source of funds, allowing us to redeploy capital into areas where we believe our bottom-up research advantage is strongest. In this way, the portfolio is gradually rotating back toward our core areas of expertise, where we believe we can generate the most value through disciplined stock selection.

Overall, the portfolio remains positioned around what we believe are some of the most durable long-term growth drivers, particularly in technology and software, while maintaining a disciplined focus on valuation, balance sheets, and downside protection.

David Barr, CFA et Amar Pandya, CFA

March 13, 2026

1 Tous les rendements signalés sont ceux des parts de catégorie F du Fonds. D’autres catégories de parts sont offertes. Celles-ci pourraient présenter des frais et des rendements différents. Les données standards sur le rendement du Fonds sont présentées ici https://penderfund.com/fr/fund/pender-small-cap-opportunities-fund/