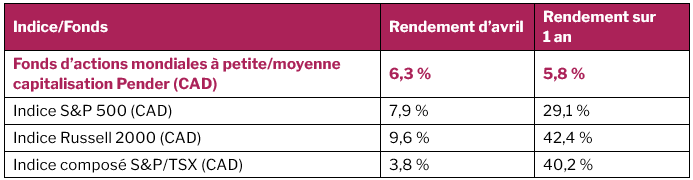

Le Fonds d’actions mondiales à petite/moyenne capitalisation Pender a rapporté 6,3 %1 en avril. Après un recul de 9,10 % depuis les hauteurs qui avait été les siennes de janvier à la fin de mars, le S&P 500 a rebondi et affiché un gain de 7,9 % ce mois-ci, allant jusqu’à atteindre brièvement un nouveau sommet historique. Trois événements convergents ont participé à cette reprise : un léger apaisement des tensions géopolitiques, des résultats financiers du T1 2026 nettement supérieurs aux prévisions des analystes et un nouvel optimisme des investisseurs envers l’intelligence artificielle qui a fait beaucoup de bien au secteur des technologies.

Les pondérations en portefeuille sont restées les mêmes : environ 49,6 % dans les actions canadiennes et 42,8 % dans les actions états-uniennes.

En avril, les titres technologiques ont été les moteurs de plus de la moitié du rendement mensuel du S&P 500, la reprise du secteur ayant germé de la récupération marquée des très grandes sociétés qui se vendaient à la baisse depuis février, moment où les inquiétudes touchant à l’IA étaient vives. Bien que les investissements colossaux dans les centres de données de l’IA ne soient pas encore totalement justifiés, les engagements en matière de dépenses en capital n’ont pas ralenti, elles semblent au contraire avoir été stimulées par l’essor généralisé du capex à travers l’économie des États-Unis.

L’industrie des semiconducteurs s’est distinguée. Advanced Micro Devices Inc. (AMD) a affiché un gain de 74,3 %, ON Semiconductor Corp. (ON) de 62,8 % et Broadcom Inc. (AVGO) de 34,9 %, hausses qui ont permis au FNB VanEck Semiconductor (SMH) de produire un rendement mensuel de 32,2 %. Alimenté par ce revirement de situation, le Nasdaq 100 s’est relevé d’environ 15 %. La demande ininterrompue des fournisseurs à grande échelle en matière de nuage et d’IA a étayé cette thématique. La croissance des actions a largement surpassé les valeurs, car les investisseurs se sont positionnés autour de ce que plusieurs appellent désormais un nouveau « supercycle de l’IA ».

Les marchés boursiers mondiaux ont connu un essor généralisé en avril. L’indice MSCI des marchés émergents a gagné entre 13,1 et 15,0 % et l’indice MSCI de l’Asie-Pacifique a bondi de 13,0 %, une hausse mensuelle inégalée depuis la fin de 2022. En effet, le cessez-le-feu au Moyen-Orient et le regain d’optimisme envers l’IA ont permis aux marchés émergents et Nord asiatiques de tirer profit d’une forte augmentation propulsée par le secteur technologique. Au Canada, la performance a été plus sectorielle. L’énergie et les biens de consommation essentiels ont résisté grâce à la remontée du prix du pétrole qui a fait contrepoids à la faiblesse du secteur des matériaux et au déclin de l’or pendant le mois.

Les résultats financiers du T1 de 2026 ont dressé un portrait en demi-teinte de la situation. Les compagnies ont fortement insisté sur leur durabilité, et plusieurs ont fait remarquer qu’à ce jour la demande était stable et que les pressions géopolitiques avaient eu peu de conséquences directes. L’IA et la construction des centres de données sont demeurés un thème positif. Toutefois, un fil de prudence s’est glissé dans la trame des commentaires. Ainsi, plusieurs équipes de direction ont qualifié le climat macroéconomique d’incertain et de dynamique tandis que beaucoup d’entreprises ont fait état de la sensibilité grandissante des consommateurs à l’inflation et au fardeau toujours présent des taux d’intérêt élevés.

Cette prudence est justifiée. Le resserrement des conditions financières causé par l’incertitude géopolitique a commencé à peser sur la croissance mondiale, et les effets indirects du prix élevé des matières premières sur la consommation sont toujours à l’œuvre au sein du système. Ce risque est démultiplié par la possibilité que l’inflation de base s’entête, tandis que la majoration de rendements obligataires pourrait amoindrir la latitude des banques centrales pour réduire les taux. En avril, la Banque du Canada, la Réserve fédérale des États-Unis, la Banque centrale européenne, la Banque d’Angleterre et la Banque du Japon ont toutes opté pour le statu quo, signe que leurs administrateurs demeurent dans l’attentisme.

Malgré tout, nous voyons quelques raisons d’être modérément optimistes. La demande industrielle a réussi à absorber une part de la mollesse des dépenses de consommation et la saison des résultats financiers a été encourageante en général. Nous continuons d’avoir confiance dans les occasions que nous identifions dans notre portefeuille et poursuivons notre répartition sélective du capital.

Mises à jour sur le Fonds (avril)

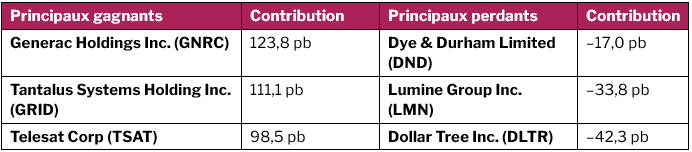

Generac a été la grande gagnante du mois. L’entreprise a publié des résultats du T1 qui surpassent les prévisions des analystes tant globalement qu’en matière de recettes. La direction a également rehaussé ses projections annuelles selon lesquelles son revenu devrait croître de 15 à 20 % et les marges de son BAIIDA excéder de 50 pb les prévisions antérieures. Le point majeur du trimestre a été ce que la direction appelle une croissance « générationnelle » sur le marché des centres de données, laquelle a donné lieu à une majoration de 28 % dans le segment commercial et industriel. Generac continue de tirer profit de la demande soutenue des clients de centres de données. Elle s’attend d’ailleurs à obtenir sous peu une première commande substantielle de la part de très grands fournisseurs, contrat qui s’ajoutera au carnet de commandes de 700 millions $ de ses services de colocation.

Tantalus s’est elle aussi très bien comportée. Ses résultats pour le premier trimestre de 2026 montrent une augmentation d’une année sur l’autre de ses revenus organiques de 27 %, des revenus de ses appareils connectés de 34 %, et des revenus de ses logiciels et services de 14 %. La compagnie a reçu, de la part de 70 sociétés de services publics, des commandes en vue de tester, de mettre en place des projets pilotes ou de déployer la passerelle TRUSense. Au trimestre dernier, elles étaient 66 à avoir passé des commandes. Environ 40 % de ces sociétés de services publics sont en phase active de déploiement.

David Barr, CFA

19 mai 2026

1 Tous les rendements signalés sont ceux des parts de catégorie F du Fonds. D’autres catégories de parts sont offertes. Celles-ci pourraient présenter des frais et des rendements différents. Les données standards sur le rendement du Fonds sont présentées ici https://penderfund.com/fr/fund/pender-global-small-mid-cap-equity-fund/