In May, the Fund returned 3.7%, ahead of the TSX at 2.5%. The S&P 1500 Software & Services Index was the standout of the month, up 14%, led by a handful of outperformers, well ahead of both the S&P 500 (+5%) and the TSX (+2.5%), marking its second consecutive month of positive returns. Even so, valuations across the software space remain depressed, as concerns about AI disruption continue to weigh on specific equities. The S&P 1500 Software & Services Index is currently trading at a 3.9x discount to its 10-year average EV/EBITDA. The selloff has pushed FCF yields higher while earnings estimates have held firm, which in our view suggests the value erosion is concentrated in terminal value assumptions rather than near-term fundamentals.

Portfolio weights remain predominantly Canadian, with approximately 81.1% in Canadian equities and 15.5% in US equities.

Geopolitical uncertainty continues to weigh on small and mid-cap equities, with the broader economic landscape still in flux. That said, markets have begun pricing in de-escalation. A credible attempt at a US-Iran agreement emerged late in May, though negotiations remain ongoing. Against this backdrop, central banks may be forced to reassess their next steps. We will note that even if the conflict were to be resolved quickly, supply chains would take months to fully recover, and logistical bottlenecks will likely continue to linger.

At the portfolio level, we're seeing a meaningful pickup in M&A activity across small and mid-cap names. Several holdings have become acquisition targets this year; a few have attracted activist attention, and others including: Kneat.com Inc. (KSI), Sangoma Technologies Corp. (STC), and Dye & Durham Ltd. (DND) have recently announced strategic reviews. We view this as an important signal: private markets are beginning to recognize value in parts of the public small and mid-cap market where valuations have remained, in our view, disconnected from long-term fundamentals. This M&A environment represents a meaningful tailwind with the potential to surface and unlock value in underappreciated portfolio companies.

Portfolio Holdings – Updates

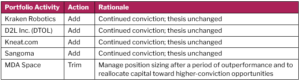

MDA Space was the top contributor in May, driven by major contract wins in the defense sector. The company continues to benefit from its strategic pivot toward high-growth areas, satellite constellations and national security, as well as continued momentum following its US listing. Given the sustained price appreciation, we trimmed the position modestly to manage sizing and reallocate capital toward higher-conviction opportunities.

Kneat.com was another standout in May. The stock rallied on two fronts during the month: first, on May 11, the company confirmed that its Board had formed a special committee to evaluate strategic alternatives, with reports mid-month indicating the bidding process had advanced to a final stage. Second, Q1 2026 results were solid, revenue of $18.0M (+22% Y/Y)2, ARR of $76.4M (+20% Y/Y), and gross profit up 28% Y/Y to $14.0M, with margins improving to 78% on cloud hosting efficiencies. Since month-end, the process has concluded: Kneat has agreed to be acquired by US private equity firm Thoma Bravo for C$650 million3, a premium of ~40% to the closing price on May 8th, the last trading day prior to the strategic review announcement. The transaction is consistent with our long-held view that the market had materially undervalued this business.

Sangoma Technologies was the largest detractor. Third-quarter results came in below Street expectations, and management lowered full-year 2026 guidance, citing geopolitical headwinds and pricing pressure in commoditized markets. The company also announced a formal strategic review to unlock shareholder value, which provided some relative support. On the leadership front, CFO Larry Stock confirmed his retirement effective June 30, with Senior VP of Finance Adrian Back named Interim CFO while the board searches for a permanent successor. Despite the challenges, our thesis is unchanged, we added to the position on weakness.

Kraken Robotics Inc. (PNG) reported Q1 results below consensus: revenue of $21.7M (+35% Y/Y) versus the Street at $25.0M (+55%)4. Full-year 2026 guidance was reiterated, and we used the share price weakness as a buying opportunity, adding to our position.

Outlook

Looking ahead, we continue to seek out undervalued small-cap businesses with what we believe are strong economic characteristics trading at attractive valuations. We are selectively adding exposure to technology companies with recurring revenue models, strong margins, and long-term compounding potential, names that have faced persistent selling pressure despite resilient fundamentals. The portfolio remains positioned around what we believe are some of the most durable long-term growth drivers, particularly in technology and software, anchored by a disciplined focus on valuation, balance sheet strength, and downside protection.

Pender Small Cap Opportunities Fund Investment Team

June 10, 2026

1 All Pender performance data points are for Class F of the Fund. Other classes are available. Fees and performance may differ in those other classes. Standard Performance Information for the Fund may be found here: www.penderfund.com/fund/pender-small-cap-opportunities-fund/

2 Kneat Announces Revenue for First Quarter, May 2026