As we find ourselves in the summer months, markets have not obliged the well-respected summer slowdown, instead greeting us with wave upon wave of volatility. Today's environment is characterized by a significant and widening bifurcation, driven by an unprecedented surge in demand for AI infrastructure and a similar acceleration in national security spending internationally. Nothing illustrates this dynamic more than the AI-linked technology sector, which now accounts for roughly 40% of the S&P 500's total market capitalization.

Portfolio weights are ~48% Canadian equities, 44% US equities and 9% international equities.

Coming back to the K-shape we've discussed in previous commentaries, the valuation disparity is, if anything, starker now. AI-focused names in the S&P 500 now trade at ~26.4x NTM earnings, against 17.5x for the index excluding those names. Meanwhile, many traditional sectors have continued trading at substantial discounts for far longer than many analysts believe to be justified. Software and commercial services names have been particularly punished, with some companies seeing NTM price-to-earnings multiples contract 50% to 70% over the past year.

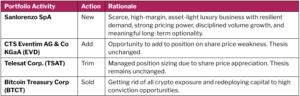

These dislocations are precisely where we may find opportunity. Our deep fundamental research approach has surfaced several potentially compelling new ideas in the international market. We recently initiated a position in Sanlorenzo SpA (SL), a name we'll discuss in further detail below.

Fund specific updates (May)

Dollar Tree was a top contributor in the month after reporting earnings that came in ahead of Street expectations, including 3.5% same-store sales growth and adjusted EPS that increased 38% year-over-year, once again demonstrating that its business model is well-suited for the current inflationary environment. The stock rose +17% on the news. Management also raised fiscal year 2026 EPS guidance by ~3%. We maintain a positive thesis on the company, its deep-value proposition and attractive opening price points enable it to better serve its core low-income customer base while also positioning it to benefit from trade-down behaviour, as consumers across multiple income cohorts become increasingly value-focused.

Kneat.com was another standout in May. The stock rallied on two fronts: first, on May 11, the company confirmed that its Board had formed a special committee to evaluate strategic alternatives, with reports mid-month indicating the bidding process had advanced to a final stage. Second, first-quarter 2026 results were solid, revenue of $18.0 million (+22% year-over-year)2, ARR of $76.4 million (+20% year-over-year), and gross profit up 28% year-over-year to $14.0 million, with margins improving to 78% on cloud hosting efficiencies. Since month-end, the process has concluded: Kneat has agreed to be acquired by US private equity firm Thoma Bravo for $650 million3, a premium of ~40% to the last trading day prior to the strategic review announcement.

Sangoma Technologies was a detractor. Q3 results came in below Street expectations, and management lowered 2026 guidance, citing geopolitical headwinds and pricing pressure in commoditized markets. The company also announced a formal strategic review, which provided some relative support. On the leadership front, CFO Larry Stock confirmed his retirement effective June 30, with Senior VP of Finance Adrian Back named Interim CFO while the board searches for a permanent successor. Despite the near-term challenges, our thesis is unchanged.

Fluor, was another detractor in the month, primarily driven by first-quarter results that came in below Street expectations and triggered an +18% stock price decline. While the company reported a return to GAAP profitability, new awards fell approximately 54% year-over-year, and management narrowed its full-year guidance range. Despite these near-term headwinds, Fluor emphasized a robust $60 billion front-end engineering pipeline and new strategic wins in the nuclear and mining sectors. Our long-term thesis on the name remains unchanged.

Sanlorenzo SpA is a new position for the Fund, adding to our international exposure, the company trades on the Milan Stock Exchange under the ticker SL. Sanlorenzo designs, manufactures, and sells made-to-measure yachts for ultra-high-net-worth individuals. This is a business that may look like a cyclical manufacturer, but we believe the business is far more durable. The company operates in a luxury oligopoly defined by what we believe to be engineered scarcity. Every vessel is bespoke. Lead times are long by design. The client base typically doesn't negotiate on price; they wait for the product. That dynamic likely insulates Sanlorenzo from the volume-driven pressures that compress margins elsewhere in industrials, and it's why we think the current valuation meaningfully underprices the business trading at 11.5X P/E.

The company was founded in 1958 and remained private for decades. Since its 2019 IPO revenues have compounded at +15% annually and EPS at +33%, with average ROIC of 17% over that same period. The balance sheet is clean; the company carries a net cash position, giving management flexibility without the leverage risk that tends to amplify cyclical drawdowns. We see Sanlorenzo as a luxury brand masquerading as a boat builder, and the market appears to be pricing it like the latter.

Pender Global Small/Mid Cap Equity Fund Investment Team

June 11, 2026

1 All Pender performance data points are for Class F of the Fund. Other classes are available. Fees and performance may differ in those other classes. Standard Performance Information for the Fund may be found here: https://penderfund.com/fund/pender-global-small-mid-cap-equity-fund/