The second quarter of 2026 saw geopolitical headlines and shifting views on technology impacting equity valuations globally. The war in the Middle East began to de-escalate by quarter-end, with Brent crude falling back to more normalized levels after peaking near US$120/barrel in April, though the full market impact is still being assessed.

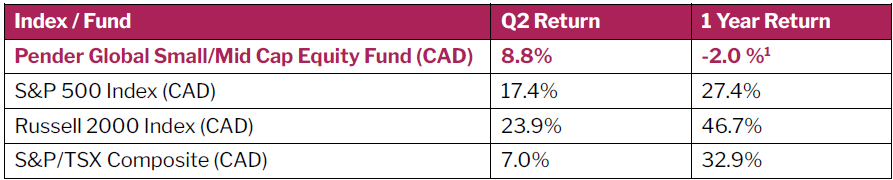

Portfolio weights are ~44% Canadian equities, 48% US equities and 10% international equities.

AI remains top of mind for investors, but a divergence is beginning to emerge within the tech sector. The Magnificent Seven have slid into negative territory YTD as a result of investor skepticism over the significant capex spend planned, as well as the extended timeline to see returns on those investments. Putting numbers to it, combined capex across Alphabet, Meta, Microsoft, Amazon, and Oracle is expected to hit roughly $750 billion in 2026, up 70% year-over-year, against expected operating cash flow of $764 billion. These are thin margins that have driven $180 billion in hyperscaler debt issuance since 2025. Google alone intends to invest up to $190 billion in capex this year, and the real question is how these companies bridge the gap until new capacity comes online: more than 60% of data centres slated for 2027 completion hadn't started construction as of May 2026, due to supply chain snags, power shortages, permitting delays, and political opposition.

Semiconductor stocks, meanwhile, rose more than 70% this quarter and 94% year-to-date, the best first-half outperformance compared to the S&P 500 in the sector's history, surpassing the prior record set during the dot-com bubble in H1 2000.

Another defining event of the quarter was the SpaceX IPO, which hit a $2 trillion valuation within days of listing, equivalent to the world's eighth-largest economy by market cap, raising the question of whether the IPO market is reopening for other large private companies. Only time will tell.

International and emerging markets had a positive but fragmented quarter. Lower crude prices helped energy-importing nations, though a strong US dollar and geopolitical uncertainty resulted in capped overall gains. Oil dropped 38% as the Iran war de-escalated and a US-Iran Memorandum of Understanding (MOU) raised hopes for reopening the Strait of Hormuz. Asia ex-Japan led at +28%, driven by Korea (+88%) and Taiwan (+49%) on semiconductor demand, while China and India lagged, this marked one of the widest geographic performance gaps in recent history. European equities rallied on Middle East de-escalation with the MSCI Europe ex-UK returning 14%.

Q2 confirmed that market leadership has broadened beyond mega-cap tech, with semiconductors' historic run and the Magnificent Seven's stumble both pointing to stock-specific drivers over index-level beta. We remain focused on quality small and mid-cap names with durable advantages and reasonable valuations, rather than capex-driven momentum that hasn't shown up in earnings. We enter Q3 constructive but selective, watching data centre buildout and currency dynamics for the next leg of divergence.

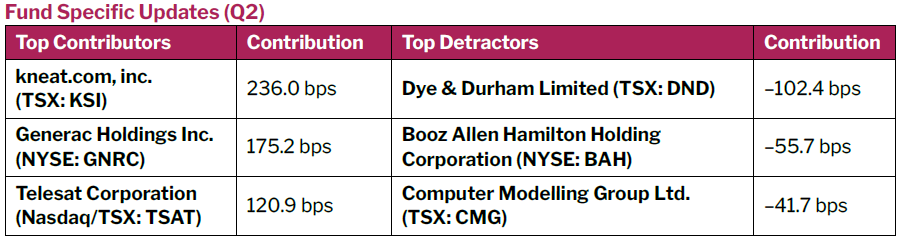

Generac was a top performing holding for the month. The company reported Q2 results that beat analyst expectations and saw management raise full-year guidance, as the company transitions from a residential-heavy focus to becoming a key provider for large-scale AI and hyperscale infrastructure.

On June 8, 2026, kneat announced it is being acquired by Thoma Bravo for $6.50 cash per share, a roughly 20% premium to last close, and a 40% premium to the unaffected price prior to the announcement of a strategic review. The transaction, although a boost to short-term performance, was not the outcome we had originally underwritten. Still, we see it as demonstrative of two things at once: just how undervalued tech remains at the smaller scale of the market, and just how active the M&A environment currently is.

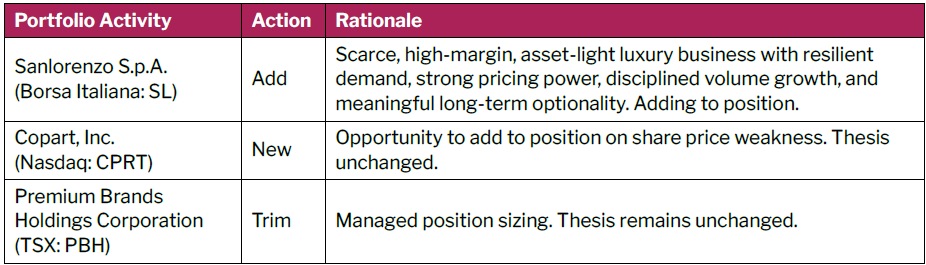

We initiated a position in Copart, Inc. (Nasdaq: CPRT). Copart is the largest salvaged vehicle auctioneer in the US, working closely with major US insurers to realize the highest value on vehicles deemed to be a total loss. The company is heavily involved in the logistics and remarketing services required to conduct a vehicle marketplace such as the transportation of vehicle to its yards and title processing. We believe the market is questioning Copart’s moat given a confluence of several negative factors that should alleviate over time. In our view, Copart offers the most liquid marketplace that enables insurers to realize the highest value on totaled vehicles, in addition to driving lowest combined ratios for these clients also through reducing administrative burdens. We believe this should sustain their market-leading position while the macro-driven impact from the personal auto industry on Copart’s growth should alleviate over time.

Pender Small Cap Equity Team

July 15, 2026

1 All Pender performance data points are for Class F of the Fund. Other classes are available. Fees and performance may differ in those other classes. Standard Performance Information for the Fund may be found here: https://penderfund.com/fund/pender-global-small-mid-cap-equity-fund/