Dear Unitholders,

The Pender Alternative Absolute Return Fund returned 0.9%1 in February, bringing year to date return to 1.3%.

Credit markets were choppy in February as elevated issuance combined with credit concerns about private debt and software companies weighed on performance. The ICE BofA US High Yield Index finished the month with a spread of 312bp OAS vs. Govt, wider by 24bp, and almost 50bp above the lows of the year reached in mid-January. A strong rally in underlying government bond yields helped partially offset widening spreads resulting in a 0.2% return at the index level. On a hedged to CAD basis, the US high yield market has returned 0.4% year to date.

The HFRI Credit Index hedged to CAD, the Fund’s benchmark, returned 0.5% in February, bringing year to date returns to 1.6%.

Portfolio & Market Update

While the market didn’t move much at the index level in February there was plenty of volatility at the individual issuer level which created trading opportunities for the Fund. We used strength to exit from some positions in retail which have historically been volatile but have seen a consistent grind higher in the current market environment. The Fund sold out of our position in Under Armour Inc. 7.25% 2030 (NYSE: UA) bonds at more than four points above par. This issue had outperformed the market this year driven by the disclosure of Fairfax’s (TSX: FFH) large equity position in the company, which triggered speculation that they could be an acquisition target.

The Fund also exited our positions in AI data center bonds following a run of strong performance. A popular trade this year has been to buy AI related issuers and sell software and other perceived AI losers including insurance brokers and in some cases media credits. We saw some opportunities to take the other side of this fairly crowded trade in February as some issuers were pushed lower than was justified by fundamentals in our view.

Much of the market that wasn’t subject to AI related concerns performed quite well in February, allowing us to take sales in some higher quality long positions which had little room for further capital appreciation.

Despite some widening from mid-January levels credit spreads remain closer to cyclical lows than cycle averages. We have seen some explanations from other asset managers about why this time might be different and we shouldn’t expect a reversion to the mean. One of the themes that comes up is that private credit has improved the pool of issuers in the high yield market. While there could be some marginal credits rated B or lower which would have otherwise come to public markets, for issuers rated BB or higher (including the entire investment grade market) there isn’t any significant difference in credit quality than prior cycles. The investment grade market in particular is dominated by the same large public issuers, although there’s been a notable increase in technology related issuance to fund the AI data center buildout, most notably from Oracle. The increased weight of Oracle does not make the case that the Investment Grade market is higher quality than it used to be, the reality is that the market quality has weakened on the margin despite spreads tightening.

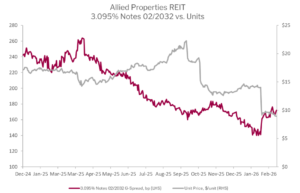

Over the past year we have seen material tightening of investment grade spreads, sometimes in the face of significant fundamental deterioration. One example of this in the Canadian Market is Allied Properties REIT (TSX: AP.UN) where poor operational and equity performance has been brushed off by the credit market and rewarded with tighter spreads.

Source: Bloomberg

We don’t see any compelling reasons why “this time is different” when it comes to higher quality credit spreads that are currently priced near historic lows.

Market Outlook

The stunning ease of Trump’s successful replacement of Maduro in Venezuela in January laid the foundation for a serious foreign policy mistake. While the small lag of a couple days between writing and publishing a commentary makes it difficult to say too much about the conflict with Iran, we believe that Trump has made a miscalculation with his attacks on Iran, which America’s own intelligence community believes is unlikely to result in regime change. While Trump has sought to create a narrative that the war is almost over likely in an effort to support financial markets, an actual offramp will prove to be difficult in our opinion.

It has been said that the first victim of war is truth, which makes it difficult to know the reality on the ground in war. But we continue to maintain a significant hedge book in risk assets as well as long in energy credits. Both of these positioning themes are driven by valuations not with the expectation of any one specific catalyst, but are well suited to an extended conflict in the Middle East.

Markets have shown a very strong impulse to buy the dip in early March. We can understand why this might be the case, with every geopolitical event that roiled markets proving to be a buying opportunity over the past year. But we also see market dynamics shifting. Supportive technicals have been met with valuation driven resistance in both equity and credit markets in recent months. We have seen some securities that were far removed from fundamental value mean revert lower in 2026.

We expect a different year for risk assets in 2026 than 2025, with so much good news already priced into valuations and a mixed bag of micro and macro events unfolding. We are expecting choppy markets and ultimately better buying opportunities in the coming months.

Portfolio Metrics

The Fund finished February with long positions of 126.1% (excluding cash and T-bills). 32.9% of these positions are in our Current Income strategy, 90.3% in Relative Value and 2.9% in Event Driven positions. The Fund had a -68.5% short exposure that included –3.8% in government bonds, -41.3% in credit and –23.4% in equities. The Option Adjusted Duration was 1.27 years.

Excluding positions that trade at spreads of more than 500bp and positions that trade to call or maturity dates that are 2028 and earlier, Option Adjusted Duration declined to 0.88 years.

The Fund’s current yield was 6.02% while yield to maturity was 6.82%.

Justin Jacobsen, CFA

March 13, 2026

1 All Pender performance data points are for Class F of the Fund unless otherwise stated. Other classes are available. Fees and performance may differ in those other classes. Standard performance information for the funds can be found here: https://penderfund.com/fund/pender-alternative-absolute-return-fund/