Dear Unitholders,

The Pender Alternative Absolute Return Fund returned 0.5%1 in December, bringing year to date returns to 2.2%.

The bid for risk in late November continued into December with equity indices, excluding Nasdaq hitting new all-time highs. The high yield market produced another positive month with the ICE BofA Index seeing spreads compress by 11bp on the month to finish at 281bp, coincidentally, spreads also finished 11bp tighter from where they started the year. The HFRI Credit Index hedged to CAD, which is the Fund’s benchmark, returned 0.7% in December, bringing 2025 returns to 7.0% 2.

Portfolio & Market Update

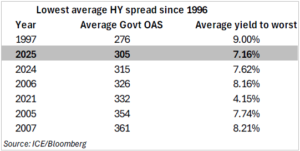

November’s brief bout of volatility was countered with strong seasonal technicals in December. Spreads are now back to levels where we believe further compression is going to be challenging as many bonds already trade at spreads that are historically quite expensive. To us, it looks like 270bp is a resistance level for high yield spreads:

Source: ICE/Bloomberg

2025 was a challenging year for the Fund. Some individual mistakes compounded a difficult macro setup with low-risk premiums with relatively limited volatility outside of a few days in April. There hasn’t been significant and tradable volatility in credit markets since the fall of 2023, which is an unusually long period of stability. We suspect that 2026 could be a year when volatility returns to markets, given how much optimism is priced into asset prices to start the year.

Using ICE/BofA data for the US high yield market which goes back to the start of 1997, no year has had a lower starting spread than 2026. While there appears to be a supportive technical “January effect” where cash is deployed into markets boosting asset prices, we view this as an opportunity to selectively trim risk into strength. We expect robust new issuance driven by attractive spreads for issuers, a need to refinance upcoming maturities and AI driven spending which has seen a steady stream of new issuing entities over the past several months.

The Fund added a new position in MDA Space Ltd. (TSX: MDA) bonds in December, a first-time high yield issuer and core holding in several Pender equity funds. The 5-year issue priced at a yield of 7% in Canadian dollars for a spread of just over 400bp. We viewed relative value as compelling, as other investors associated the business with troubled satellite issuers, rather than a nationally strategic defense business. Since the issuance of the bond in early December there have been several positive business announcements from the company which has caused the bond to rally above issuance price, benefiting the Fund.

The Fund’s two small individual equity shorts were negative contributors to the Fund in December. At the outset of the month the combined position sizes for these two holdings was less than 1% of the Fund’s NAV. There was a strong technical bid for both issues, which created opportunities for us to tactically add exposure. Both equities saw capital gains in 2025 despite in both cases operating results coming in well below expectations at the outset of the year. We believe this speaks to the general tone and vulnerabilities embedded in asset prices today, where good news is rewarded and, in many cases, negative results are glossed over. We are very careful about how we manage short exposures, especially in individual securities that are prone to volatile moves. We believe it’s important to respect technicals but also maintain a keen focus on fundamental value especially when prices are highly dislocated from that value. One of our equity shorts currently trades at between double and triple what we believe fair value is, presenting a compelling short opportunity over the longer term.

The Fund remains conservatively positioned to start 2026, as our focus is on finding quality short duration positions to generate carry and on what we expect to be a busy new issue calendar to start the year. While opportunities are limited, there are situations where investors are paid enough to take some risk and we saw opportunities to add to exposures yielding between 8-9% in USD early in the new year.

Market Outlook

High yield returns in 2025 benefitted from both lower government bond yields and tighter spreads but most of the compression in market yields came from the Treasury market, where the key five-year yield dropped from 4.4% to 3.7% over the course of the year. For another similar drop in government yields, we believe that there would need to be significant economic weakness, which would likely result in higher spreads than current levels.

Source: ICE/Bloomberg

As a base case we would expect the high yield market to generate lower returns in 2026 than 2025 driven by a lower starting yield and limited room for spread compression.

Risks tend to build up over long periods of rising asset prices and low volatility. We believe that valuations that aren’t likely to be backed up by cash flows in coming years are one of the largest sources of risk in markets today. This is particularly true for anything associated with AI, as the narrative of future growth has been the dominant driver rather than results or business models being proven.

In January 2026, Bloomberg reported that Elon Musk’s xAI had successfully raised $20 billion in a Series E funding round, valuing the business at $230 billion, an increase of more than 50% from a funding round in mid-2025. This increase in valuation occurred despite the fact that the business is highly unlikely to meet the 2025 financial projections issued in the middle of last year, with lower revenues and wider losses. Rising asset prices in the face of subpar results is hardly isolated to venture and private markets. Over the past two years, Tesla’s equity price has roughly doubled, while the consensus estimate for 2026 EBITDA has been cut in half. While this is a particularly extreme example, there are plenty of other companies where equity prices and earnings estimates have moved in opposite directions over the past year.

The circularity of the AI financing ecosystem has continued to grow into 2026. News articles reported that Nvidia contributed as much as $2 billion of the xAI Series E financing, increasing their exposure further by contributing equity capital to a Special Purpose Vehicle (SPV) backed by Valor Equity Partners to buy $5.4 billion of their own chips for xAI’s data centers. While AI infrastructure spending continues to grow, the ultimate business models of the software businesses are largely unproven, while revenue growth looks to be already falling behind lofty expectations for several leading companies.

The dramatic increase in credit markets exposure to the AI data center buildout since September will likely continue to create both volatility and trading opportunities in 2026. While retail investor enthusiasm remains high for many AI-related businesses, there was large insider selling of Coreweave (Nasdaq: CRWV) on December 24, well below mid-January trading levels of the stock.

Geopolitical risk has been largely brushed aside by markets in recent years, but that could change in 2026. Increasing inequality combined with frustration with the past several years of elevated inflation could result in both a “blue wave” and a rise of populism in the US midterm elections this year which would likely be viewed negatively by markets.

In early 2026 risk markets feel almost unstoppable, but history has shown that markets eventually mean revert, and periods of extremely buoyant sentiment often occur close to market peaks. We would like to thank our valued clients for their patience and are optimistic that 2026 will provide better opportunities for the Fund.

Portfolio Metrics

The Fund finished December with long positions of 126.5% (excluding cash and T-bills). 28.1% of these positions are in our Current Income strategy, 98.4% in Relative Value and 0.0% in Event Driven positions. The Fund had a -67.1% short exposure that included –3.8% in government bonds, -40.5% in credit and –22.8% in equities. The Option Adjusted Duration was 1.85 years.

Excluding positions that trade at spreads of more than 500bp and positions that trade to call or maturity dates that are 2028 and earlier, Option Adjusted Duration declined to 1.39 years.

The Fund’s current yield was 6.36% while yield to maturity was 6.98%.

Justin Jacobsen, CFA

January 22, 2026

1 All Pender performance data points are for Class F of the Fund unless otherwise stated. Other classes are available. Fees and performance may differ in those other classes. Standard Performance Information for Pender’s Liquid Alternative Funds may be found here: https://penderfund.com/fund/pender-alternative-absolute-return-fund/

2 Benchmark HFRI Credit Index and ICE/Bloomberg