January was characterized by a sharp shift in investor sentiment, particularly toward growth-oriented sectors. As markets reassessed expectations around artificial intelligence, concerns that AI could materially disrupt traditional software business models resurfaced and weighed heavily on software equities. This narrative assumes that enterprises will increasingly rely on internally developed AI tools rather than purchasing software from established providers. We view this assumption as overly simplistic, given the complexity, regulatory requirements, and mission-critical nature of most enterprise software platforms. Even Nvidia CEO Jensen Huang recently described the notion of AI “killing software” as “the most illogical thing in the world”, reinforcing our view that durable software franchises remain well positioned despite near-term sentiment pressures.

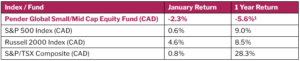

Against this backdrop, the Pender Global Small/Mid Cap Equity Fund declined 2.3% during the month. Given the Fund’s exposure to information technology and software (approximately 26%), the broad-based drawdown in software equities had a meaningful effect on short-term performance. Importantly, this pullback was largely sentiment-driven and reflected valuation pressure rather than a deterioration in revenues or cash flow generation across the Fund’s core software holdings.

It's worth highlighting that the market has treated software businesses as largely interchangeable, failing to distinguish between fundamentally different business models. Vertical market software companies serving niche markets, characterized by high switching costs, recurring revenues, and pricing power have sold off alongside more cyclical or discretionary software businesses.

This pullback created an opportunity to redeploy capital where the gap between price and intrinsic value widened meaningfully. We took advantage of this dislocation by adding to high-conviction holdings and initiating new positions at more compelling valuations, reflecting our view that the opportunity set within software is improving rather than deteriorating.

The current environment is more complex than in recent periods. While near-term uncertainty remains elevated, we believe attractive opportunities are beginning to emerge for disciplined investors focused on fundamentals and long-term value creation.

Portfolio weights remained approximately 58.3% Canadian equities and 40.2% US equities.

Fund specific updates (January)

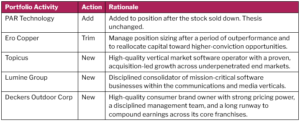

This month, we were active in the portfolio, taking advantage of opportunities created by the sell-off in the software sector. Notably, we initiated new positions in Topicus.com Inc. (TOI)and Lumine Group Inc. (LMN), both of which are spin-outs of Constellation Software Inc. (CSU).

As a reminder, Constellation Software’s long-standing strategy has been to acquire small, niche vertical market software businesses with high pricing power, integrate them into a decentralized operating structure, and generate resilient cash flows from sticky customer bases. Following its success, Constellation separately listed two former subsidiaries: Topicus.com in 2021 and Lumine Group in 2023. Both companies continue to follow a disciplined, acquisition-led model informed by Constellation’s operating playbook, while pursuing independent growth strategies. Lumine Group focuses on acquiring, strengthening, and growing vertical market software businesses within the communications and media industries. Topicus.com focuses on acquiring and operating vertical market software businesses across Europe, serving mission-critical needs in both public and private sector end markets.

These are high-quality software businesses that we believe are currently being overly penalized by the market. In our view, investors are pricing in overly pessimistic scenarios, despite the resilient, mission-critical nature of the end markets served by businesses such as Topicus and Lumine. While uncertainty has driven sharp share price movements, such dislocations often create attractive entry points. As a result, select software companies with durable recurring revenues, disciplined acquisition strategies, and long-term growth runways are trading at valuations that, in our opinion, do not fully reflect their underlying business quality or long-term potential.

We also initiated a new position in Deckers Outdoor Corp (DECK), a global leader in innovative footwear, apparel, and accessories for both everyday lifestyle and high-performance. The company’s portfolio includes UGG, HOKA, and Teva. Deckers has demonstrated a proven ability to build niche footwear brands into global lifestyle leaders with highly loyal consumer bases. Deckers benefits from a long runway to deploy capital at high rates of return (30%+), particularly in areas such as sales and marketing, innovation in new footwear categories, and through the natural replacement cycle within the running shoe category, which supports durable, recurring demand. We view Deckers as a high-quality, high-return business with strong cash flow generation and long-term compounding potential, well aligned with our investment philosophy.

David Barr

February 19, 2026

1 All Pender performance data points are for Class F of the Fund. Other classes are available. Fees and performance may differ in those other classes. Standard Performance Information for the Fund may be found here: https://penderfund.com/fund/pender-global-small-mid-cap-equity-fund/