Dear Unitholders,

The Pender Alternative Absolute Return Fund returned 0.4%1 in January.

Robust inflows into risk assets drove returns in January, with the first two weeks of the year being particularly strong. The ICE BofA US High Yield Index reached a spread of 264bp Govt OAS mid-month before widening to finish the month at 288bp Govt OAS, a slightly higher spread than the start of the year. The investment grade market performed better on a spread basis in January, finishing the month tighter with the primary ICE BofA Corporate Index reaching its lowest spread level since 1998 late in the month.

The HFRI Credit Index hedged to CAD, the Fund’s benchmark, returned 1.1% in January.

Portfolio & Market Update

The month of January, in particular the first two weeks of the year, is usually a particularly strong period for the high yield market driven by inflows into the asset class. This year was no different but driven by stretched valuations it was difficult for the market to hold those gains, with the high yield market producing a negative return in the second half of the month.

Despite expensive valuations which didn’t change much at the index level, we saw increased trading opportunities in January. A new issue from a subsidiary of Six Flags Entertainment Corp. (NYSE: FUN) provided trading opportunities in both existing bonds and the new issue, resulting in gains for the Fund. The six-year unsecured issue was priced at a yield to maturity of 8.625% and finished the month about two points above par.

The American intervention into Venezuela caused spreads to widen for bonds issued by Canadian oil and gas producers in January which allowed us to add to our position in Vermilion Energy Inc’s 7.25% 2033 bond at a yield to maturity of about 8.5%. Following a more sober reassessment by the market about the challenge of ramping Venezuelan oil production as well as likely limited impacts on Canadian producers, the sector rallied with Vermilion’s bond participating and closing the month about three points higher than our purchase price to yield less than 8% to maturity.

Another area where we saw an opportunity was in bonds issued by a subsidiary of Charter Communications (Nasdaq: CHTR). Over the past couple of years cable multiples have re-rated lower. Charter has acknowledged this reality and lowered their leverage targets starting early last year. With negative sentiment going into their quarterly results, compounded by a difficult quarter for their largest competitor, Comcast, we built a position in six- and seven-year maturities that performed well following better than expected quarterly results and a further commitment to lowering leverage.

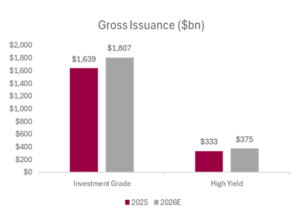

January saw surprisingly little AI related issuance as we didn’t see any issuance in investment grade or high yield markets. February started with a bang as Oracle issued $25 billion in bonds to fund their data center buildout on the first business day of the month, with additional IG, high yield and ABS issuance taking the total to almost $50 billion in US credit markets in the first half of the month. With large tech companies continuing to raise their capital expenditure budgets, we anticipate a very strong year for issuance in 2026. JP Morgan is projecting record investment grade issuance and a noticeable uptick in high yield issuance this year. With about $300 billion of IG issuance relating to AI infrastructure.

Source: JP Morgan

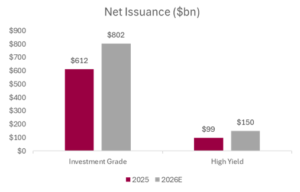

Note: Net issuance is new issues less the cash generated from maturing bonds.

Impressive advances in AI, particularly by Anthropic’s Claude, have prompted significant investor fear towards software companies coupled with a renewed enthusiasm for AI including data centers. As recently as November circular financings were causes for concern, while in January circular financings like Nvidia’s equity investment into high yield “neo cloud” operator Coreweave Inc. contributed to market rallies. We used strength to sell down some of our data center exposures in the Fund. In early February the Fund initiated a long position in a high-quality software issuer where relatively short-term bonds had widened to spreads that exceeded the post Liberation Day sell off in April 2025.

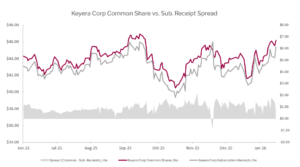

We’ve been building out an attractive arbitrage position in the Fund in Keyera Corp. subscription receipts (TSX: KEY/R) using Keyera common shares as a hedge. The subscription receipts will convert to common shares once the company’s acquisition of Plains All American’s (NYSE: PAA) Canadian assets closes, which the company expects to occur this quarter. Usually in merger arbitrage situations with a high probability of closing, spreads compress with the passage of time. That has not been the case for Keyera receipts, which have frequently traded at about a 2-3% discount to Keyera common in recent weeks, with the transaction likely to close within the next two months we view this spread as a compelling use of capital. A Canadian company purchasing Canadian assets from a US operator who was unlikely to invest significant capital into them aligns perfectly with Canada’s stated priorities. With the transaction fully financed, the only obstacle to closing is federal regulatory approval.

Source: Bloomberg

The primary detractors of the Fund’s performance in January were our hedges. With relatively few market moving news events in the month, strong inflows into risk assets were the dominant factor driving asset prices higher. Even in a robust year for risk assets and credit like 2025, the lowest spread for the year in high yield was reached in January. We wouldn’t be surprised if the same was true in 2026. We expect that our defensive positioning should serve us well in the coming months as inflows into risk assets are likely to moderate and issuance appears to be ramping up, which should result in more trading opportunities for the Fund and more volatility for broad markets.

Market Outlook

Beneath the surface of markets near cyclical lows in credit spreads and all-time highs in equities is increasing dispersion between how the market treats individual companies and issuers. We believe that the resulting increase in opportunities for the Fund is likely to continue.

Considering several broad equity indices are trading around the same levels as late October despite coming through a seasonally strong period does not bode well for near-term returns in our opinion. Valuations are a clear headwind to risk assets. Speculative assets like silver, which was effectively turned into a meme stock in recent months starting to mean revert is also an indication that market dynamics are shifting.

A very strong three years for risk assets have embedded a lot of complacency into historically low risk premiums. Complacency leads to sharp reversals once a risk has been identified, which is what we have seen in software credits and equities in recent weeks. We expect more sector or thematic risk events in the coming months. One area where we see high levels of complacency is in investment grade rated credit in Canada. In some cases, investors have relied on a single credit rating from DBRS to adjudicate risk and have taken spreads tighter over the past year despite clear evidence of fundamental deterioration.

Momentum has been a defining characteristic of price movements in markets for much of the past year, with little regard for valuations and sometimes even fundamentals. A pivot towards mean reversion bodes well for our approach to investing. Even in 2025, which saw the lowest average spread for the high yield market since 1997, spreads were higher on average than they are today. Considering all the cracks forming in markets, we expect a higher average credit spread this year than last.

Portfolio Metrics

The Fund finished January with long positions of 124.4% (excluding cash and T-bills). 30.5% of these positions are in our Current Income strategy, 92.1% in Relative Value and 1.8% in Event Driven positions. The Fund had a -68.5% short exposure that included –3.8% in government bonds, -41.1% in credit and –23.6% in equities. The Option Adjusted Duration was 1.55 years.

Excluding positions that trade at spreads of more than 500bp and positions that trade to call or maturity dates that are 2028 and earlier, Option Adjusted Duration declined to 1.10 years.

The Fund’s current yield was 6.15% while yield to maturity was 6.88%.

Justin Jacobsen, CFA

February 23, 2026

1 All Pender performance data points are for Class F of the Fund unless otherwise stated. Other classes are available. Fees and performance may differ in those other classes. Standard performance information for the funds can be found here: https://penderfund.com/fund/pender-alternative-absolute-return-fund/