CIO’s Commentary – Felix Narhi

“Markets are constantly in a state of uncertainty and flux and money is made by discounting the obvious and betting on the unexpected.” – George Soros

In this commentary we cover:

- Looking back at the last decade

- Today’s record US bull market

- Everything is (still) cyclical

- Looking forward to the next decade

- Past cycles may hold some clues for the future

- Bet on the unexpected

Considering the elevated investor fear levels in December 2018, few would have predicted that in less than a year the S&P500 would surpass all previous rallies to become the best performing bull market since World War II. Yet here we are. If you invested in the S&P500 in 2009, then it has been a wondrous ride (assuming you stayed the course and did not panic during the numerous times when fear overtook the market). As we near the close of the decade we take a pre-emptive look back at this high-flying US market and the potential lessons for the future.

LOOKING BACK AT THE LAST DECADE

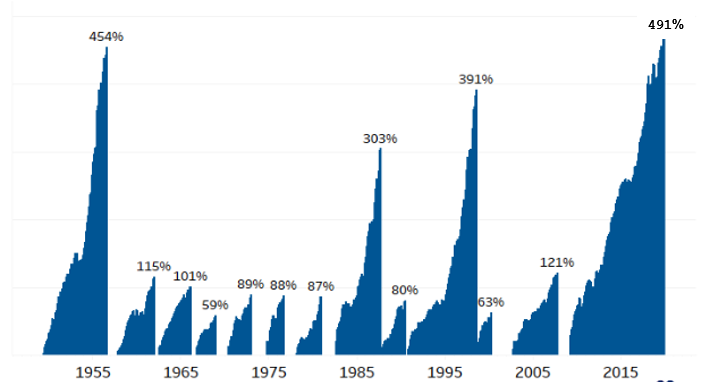

Today’s Bull Market is the Best Performing and Longest Ever (and still counting!)

S&P500 total return (last period 3/9/09 to 12/17/19)

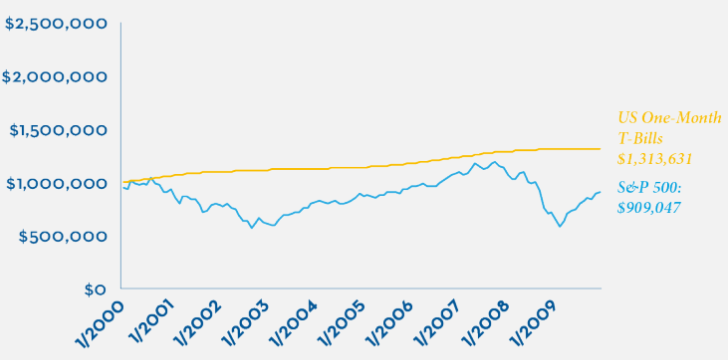

The Lost Decade

As we look forward, it’s worthwhile trying to step back into the typical investor’s mindset in December 2009 as she might have thought about navigating the markets. Indeed, it is hard to even remember how different the market environment was back then. Following the fabulous bull market and optimism of the 1990s, American investors had lived through two recessions, including the worst economic crisis since the Great Depression. This led to two massive stock market crashes which saw stocks drop by half each time. The S&P500 had plenty of ground to cover following its “lost decade” from January 2000 to December 2009. Over that period the US stock market posted a negative total return of 9% including dividends. It was even worse if you were a Canadian investor because currency related headwinds further lowered your return as the US greenback depreciated relative to the loonie. Measured in Canadian dollars, the S&P500 was down 34% for the decade. Ouch. Wall Street had a huge party back in the halcyon dotcom days of 1999, but the hangover proved to be proportional to the binge. Not surprisingly, there was little enthusiasm for the S&P500 after such a long period of terrible performance. The obvious bet? Just avoid the S&P500.

The Lost Decade

S&P500’s miserable decade from 1999-2009

Yet, this was the eve of the S&P500’s GREATEST.RUN.EVER. Few could have predicted the incredible outperformance of the S&P500 in the ten years since, especially relative to other global markets (we certainly didn’t!).

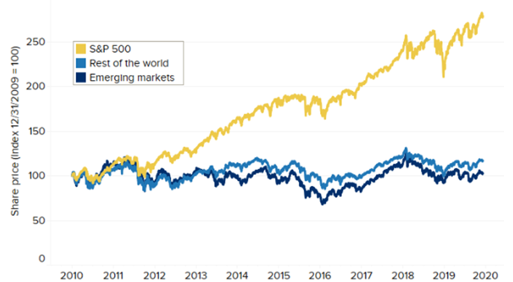

An American Renaissance followed the Lost Decade

S&P500 more than making up for lost time…

Indeed, the playbook that had worked best in the previous decade flipped. Large US stocks have trounced most global markets and asset classes over the last decade. Stock selectors seeking opportunities outside the S&P500 have faced a decade long headwind. The continued favourable momentum in US large caps have attracted record levels of inflows into the S&P500-related index funds and ETFs. It is only human nature to chase past returns.

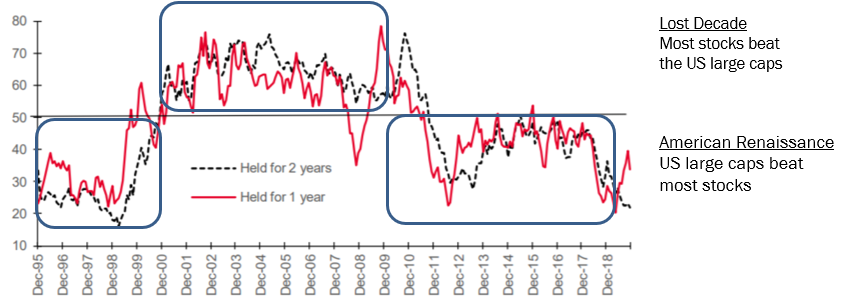

Everything is (still) Cyclical

Percentage of global stocks out of a universe of 16,000 world stocks outperforming the S&P500 over a one and two-year basis

If you can’t beat em, join em?

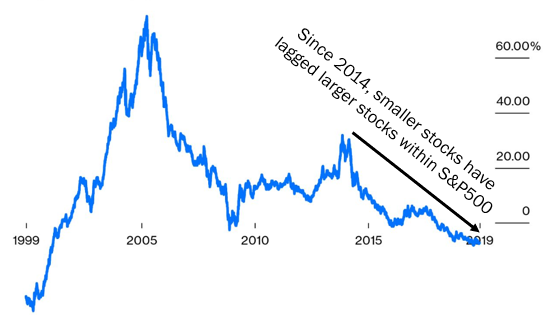

Indeed, it has been an American Renaissance decade with it record bull markets. One of the few ways to beat the large cap US stocks over the last decade was to go even bigger. The more mega, the more the lucrative, particularly of late. If you had been overweight in the 50 largest US companies in the S&P500 since 2014, you would have comfortably outpaced the S&P500. Today, the top ten largest companies in the S&P500 equate to 25% of the total index’s value, while the top 46 largest stocks are half the entire index’s value. If this trend continues, the market will become narrower, as fewer and fewer companies will carry more and more of the weight to drive the broad US market returns higher. Today’s consensus “TINA” (There Is No Alternative) trade on the S&P500 is really a bet on the continued outperformance of these megacaps. We are less sure than the consensus that this trend will continue. We have been through a number of different cycles which has taught us “this too, shall pass”. Importantly, we believe there are alternatives.

Megacaps have outpaced the average stock in the S&P500 since 2014

Rolling 5-year return of equal-weight S&P500 relative to capitalization weight S&P500 (%)

LOOKING AHEAD TO THE NEXT DECADE

“Humans are prone to herd because it is always warmer and safer in the middle of the herd. Indeed, our brains are wired to make us social animals. We feel the pain of social exclusion in the same parts of the brain where we feel real physical pain. So being a contrarian is a little bit like having your arm broken on a regular basis.” – James Montier

Today’s obvious bet is to buy US megacaps. Or is it? Let’s further unpack the last decade to see if we can learn anything from history and see if there might be some clues for the future.

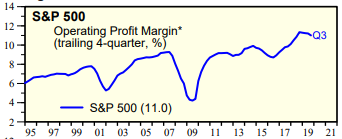

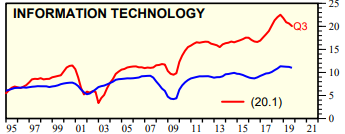

While valuation levels expanded over this period, it turns out that the outperformance of US stocks was mostly driven by strong underlying business fundamentals. It has been a period of unusually robust earnings growth, up 179%, or nearly 11% annualized, over the last decade. This was driven by mid-single digit revenue growth and impressive margin expansion which was the result of several factors.

At the start of the decade, earnings were driven by the recovery following the Great Recession, which was aided in part by an unprecedented monetary easing by central banks. More recently, US corporate profitability was boosted by Trump’s Tax Law, signed at the end of 2017, which cut corporate tax bills nearly in half. According to a recent study, American corporate tax rates are now at their lowest level in nearly four decades. Both of these factors have boosted earnings growth, but are likely one-time in nature. With global rates at all-time lows, quantitative easing has reached the end of its effectiveness. In addition, the US economy, widely lauded as very strong, is at peak performance from a cyclical standpoint, so any change is more likely to be to the downside. Finally, now that corporate tax rates are at 40-year lows, further tax relief from Uncle Sam is out of the question. However, relative to the world, the US market has benefited from a unique advantage which is structural: it is the home of most of the world’s most powerful and ubiquitous tech companies.

In aggregate, the info tech sector has grown much faster than the rest of the market. Tech leaders in particular are incredibly profitable. By market capitalization, the five largest tech companies in the world are Apple, Microsoft, Alphabet, Amazon and Facebook and all are listed on the S&P500. The next two largest tech firms are Alibaba and Tencent, both based in China. Increasingly, tech leaders are winning the game in almost every industry. The “moats” or competitive advantages of yesteryear which were built through large investments in industrial plants, buildings and retail networks are increasingly being wiped out, replaced by new capital-light business models. As legacy business models lose out in the US, these tech giants often step in. In most other global markets, there are far fewer large tech leaders to fill the gaps in their respective stock markets when the old guard loses their relevance. In many cases, market capitalization of failing local players is transferred from regional stock markets into the S&P500. This headwind for local markets becomes a tailwind for the US market as industry profit pools shift. The operating margins of tech giants have soared over the last decade and pushed margin aggregate levels well above normalized cyclical levels. Is it sustainable? It might be if it’s structural.

US large cap margins near record levels (11%)… Driven by rising Info Tech sector margins (20%)

Source: Yardini

“Faced with the choice between changing one’s mind and proving there is no need to do so, almost everyone gets busy on the proof.” – John Kenneth Galbraith

Reversion to the mean, a long-time statistical phenomenon is not dead, but clearly there is something else going on. As we have noted, we are living in new world where many of the largest global companies operate with immaterial amounts of tangible capital. Yet these companies continue to generate growing amounts of recurring free cash flows. This is unprecedented. The margins of such companies may be structurally higher than in the past. Hard book value as an indicator of intrinsic value is increasingly irrelevant because the world has changed. According to a study by Harris Associates, the co-relation between book value and economic value has been broken. In 1975, the correlation between stock price and tangible book value for the largest S&P500 companies was 71%. Today, it is 14%. Buying a cheap price-to-book value stock and hoping that mean reversion will carry the day is a foolhardy exercise in those cases where tangible capital is no longer a competitive advantage or a relevant driver of economic performance. Of course, there are many sectors where tangible capital still matters, like real estate and banking. But in aggregate, it will probably be a mistake to bet against the ascendance of intangible assets in the coming decade as technology becomes increasingly pervasive in society. Many investors have been caught off guard by these structural changes in the economy.

The Unexpected

“Be extra careful when buying into companies and industries that are the current darlings of the financial community.” – Philip Fisher

The S&P500 followed one of its worst decades on record in the 2000s with one of its best in the 2010s, on both an absolute and relative basis. The S&P outperformed the vast majority of asset classes and global markets over that period. We believe technology will remain an important structural theme for the foreseeable future, but the leadership could change. IBM was a top ten S&P500 stock in 2009, but fell off this past decade when it focused more on financial engineering rather than actual engineering and innovation. And it took Microsoft 16 years to pass its previous peak stock price high in 2000 despite impressive business growth during that period. Price matters. What could become of our current cohort of the market’s much-loved tech leaders this coming decade? Could the playbook flip again?

The last decade has taught us that outperformance tends to occur when investors have low expectations, where operating margins start at depressed levels and where the potential runway is long, like the global markets which have opened up for borderless companies like Facebook and Alphabet. These companies posted their best returns when they were smaller and younger and had the most room to grow. It’s harder to grow as fast when you become larger and dominate your industry. Today’s US megacaps are the current darlings of the financial community, and the obvious bet, which warrants some extra caution, particularly now that those stocks are driving the world’s best and longest performing stock market. We have seen time after time that the markets are still cyclical.

Predicting the future is hard, if not impossible, but looking back ten years from now, we would imagine that many of the best performing stocks would share some similar attributes that led to this last decade’s best performers. Most of the winners would have started the period with low investor expectations and valuations, modest initial operating margins with plenty of room for improvement, and with a much smaller market capitalization with the potential to become much larger over the coming decade. In short, the opposite of today’s S&P500. We think it is therefore reasonable to believe that many of today’s less loved smaller capitalization stocks will once again shine in the coming decade.

Investing is a probabilistic endeavor. When it comes to market returns, no one knows what the next decade holds for investors. If history is any guide, the next 10 years are likely to look nothing like the last 10 years. Future generations will no doubt look back on the historic record-breaking US bull run and conjure up valuable lessons that only come with hindsight. But a sound starting point might be to bet on the unexpected and discount the obvious.

Please do not hesitate to contact me, should you have questions or comments you wish to share with us.

Felix Narhi

December 20, 2019